If you’ve used no-KYC crypto cards for any length of time, you’ve seen it: a card works perfectly for months, then one day — dead. No warning, no explanation, just a frozen balance and a vague email about “compliance requirements.”

This isn’t random. There’s a structural reason no-KYC crypto cards face constant shutdowns, and understanding it helps you protect your money.

The Core Problem: Card Networks vs. Anonymity

Every no-KYC crypto card that works at real merchants uses the Visa or Mastercard network. These aren’t optional partnerships — without Visa/MC, a card is just a number on a screen.

Both networks require their issuing partners to follow strict anti-money-laundering (AML) and Know Your Customer (KYC) regulations. Programs that don’t comply face termination.

No-KYC crypto cards exist in the gap between what card networks require and what issuing banks actually enforce. When the network audits and finds non-compliant programs, they pull the plug.

This is the fundamental tension: the product (anonymous spending) conflicts with the infrastructure (regulated card networks). Every no-KYC card is operating on borrowed time until compliance catches up.

The 5 Reasons Cards Get Terminated

1. Card Network Audits

Visa and Mastercard run regular compliance audits on their issuing partners. If they discover a program issuing cards without proper KYC, they can terminate the partnership. This is the most common shutdown trigger.

2. Regulatory Enforcement

Governments are tightening crypto regulations globally. The EU’s MiCA framework, the expanding Travel Rule, and individual country enforcement actions put pressure on card issuers. Some jurisdictions have made it explicitly illegal to issue payment cards without identity verification.

3. Bank Partner Withdrawal

The issuing bank (which holds the actual Visa/MC license) can decide the risk isn’t worth it. If their compliance team flags a no-KYC card program, they can sever the relationship. The card provider loses their banking rails overnight.

4. Fraud and Abuse Accumulation

No-KYC cards attract a disproportionate amount of fraud — stolen crypto, money laundering, and sanctioned transactions. When fraud rates exceed thresholds, card networks intervene.

5. Competitor Reporting

Yes, this happens. Competing card providers (especially KYC-compliant ones) sometimes report non-compliant programs to regulators or card networks. It’s a way to eliminate competition through regulation.

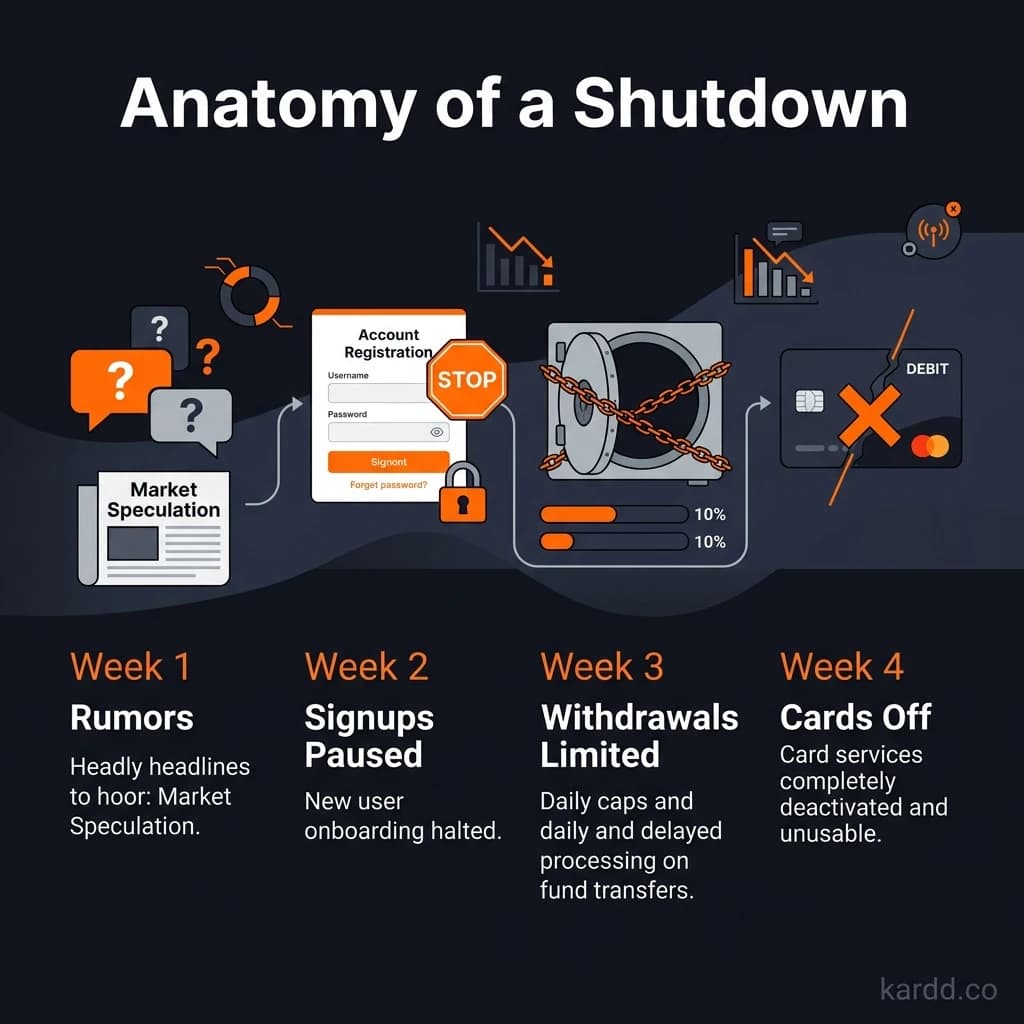

What Happens When a Card Shuts Down

The typical timeline:

Day 0

Card stops working. Transactions decline at the point of sale.

Day 0-3

Provider sends an email or dashboard notice. Sometimes vague (“service discontinued”), sometimes specific (“regulatory requirements”).

Day 1-7

Existing balances are frozen. You cannot withdraw or spend remaining funds.

Day 7-30

Provider may offer a voluntary KYC process to recover funds. Submit ID, get your balance back. Some users do this; others walk away.

Day 30-180

If you don’t complete KYC, funds sit frozen. Most providers eventually return funds to the original crypto address — minus processing fees (typically 5-10%).

Worst case

Provider disappears entirely. Unregulated operators have no legal obligation to return funds. Your loaded balance is gone.

Notable Shutdowns and What We Learned

The no-KYC card space has a graveyard of former providers. Patterns emerge:

Cards that died fastest were typically:

- New providers with less than 6 months of operation

- Programs offering unrealistically low fees (below cost)

- Cards with no clear banking partner

- Providers that didn’t adapt when regulations changed

Cards that survive longest tend to:

- Operate through established, diversified banking partners

- Adjust their KYC tiers proactively (adding optional verification)

- Maintain transparent communication with users

- Have revenue models that don’t depend solely on card issuance

How to Protect Yourself

Rule 1: Never keep more than you’ll spend in the next 3-5 days.

This is the single most important rule. If a card shuts down tomorrow, you lose only a few days’ spending money — not your savings.

Rule 2: Diversify across 2-3 active cards.

If one dies, you have backup spending options while you find a replacement. Kardd.co tracks 11 active cards — spread across providers in different jurisdictions.

Rule 3: Check card status before loading.

Kardd.co updates weekly. Before any large load, check that your card is still operational and hasn’t reported issues.

Rule 4: Keep records of all funding transactions.

Screenshot every deposit address and transaction hash. If a card freezes and offers KYC recovery, having proof of funding helps. If the provider disputes ownership, blockchain records are your evidence.

Rule 5: Prefer established providers.

Cards with 6+ months of continuous operation and transparent banking partners are lower risk. New cards with amazing deals are higher risk.

Which Cards Are Most Stable?

Kardd.co ranks cards into three tiers partly based on operational stability:

Gold Tier (most stable)

- XKard — Longest operational track record among zero-KYC cards. Multiple banking partners. Proactive tier system.

- SolCard — Solana ecosystem integration provides additional revenue stability.

Silver Tier (established)

- BingCard, KAST, COCA Card, Laso Finance — Operating for several months with consistent service.

Bronze Tier (newer/higher risk)

FAQ

Will all no-KYC crypto cards eventually shut down?

Not necessarily all, but the landscape will keep shrinking as regulations tighten. Cards that adapt — adding optional KYC tiers, diversifying banking partners, operating in crypto-friendly jurisdictions — have the best chance of surviving long-term.

Can I get my money back from a shut-down card?

Usually yes, but with delays and fees. Most providers return funds to the original crypto address within 30-180 days after deducting a processing fee (5-10%). If the provider disappears entirely, recovery is unlikely.

Are there warning signs before a shutdown?

Sometimes. Watch for: unexplained transaction delays, temporary “maintenance” windows that keep extending, loss of mobile pay support, and sudden fee increases. Kardd.co flags these early warning signals.

Is it safer to use a partial-KYC card instead?

Partial KYC (phone verification) does reduce shutdown risk slightly — it shows the provider is making some compliance effort. But it doesn’t eliminate the risk. Even partial-KYC programs can be terminated by card networks.

Conclusion

No-KYC crypto cards operate in inherent tension with the regulated card networks they depend on. Shutdowns are a feature of the landscape, not a bug. The best strategy is: keep low balances, diversify providers, and stay informed.

Check current card status

Kardd.co tracks operational status, shutdown warnings, and stability ratings weekly.

Check Status on Kardd.coCards Mentioned in This Guide

Last verified: March 18, 2026. Card details, fees, and KYC requirements may change without notice. Always verify current terms directly with the card issuer before loading funds. Kardd.co is an independent comparison site — we are not affiliated with any card issuer except through publicly available affiliate programs. Full affiliate disclosure