No-KYC Crypto Card vs KYC: What's the Real Difference?

You want to spend crypto in the real world. You load up a card comparison site, and every listing hits you with the same fork in the road: no KYC vs KYC crypto card — submit your passport and selfie, or skip verification entirely.

One path promises privacy. The other promises stability. Both come with trade-offs that most guides gloss over. This article breaks down every meaningful difference so you can pick the right card for how you actually spend.

What Is a KYC Crypto Card?

A KYC (Know Your Customer) crypto card works like a traditional bank-issued debit card. Before you can load funds or make purchases, the issuer verifies your identity — typically through a government-issued ID, proof of address, and sometimes a live selfie.

Cards from providers like Coinbase, Crypto.com, and Binance all require full KYC. Once verified, you get higher spending limits, chargeback protections, and access to features like direct bank withdrawals.

The trade-off is straightforward: you hand over personal data in exchange for a more traditional banking experience layered on top of crypto.

What Is a No-KYC Crypto Card?

A no-KYC crypto card lets you load cryptocurrency and spend it anywhere Visa or Mastercard is accepted — without submitting identity documents. You sign up with an email address (sometimes just a crypto wallet), fund the card, and start spending.

These cards exist because a significant portion of crypto users value financial privacy. They are not inherently illegal, but they operate in a regulatory gray area that varies by jurisdiction.

We maintain a full ranking of the best options in our Best No-KYC Crypto Cards for 2026 guide. The short version: the market has matured significantly, and several no-KYC cards now support Apple Pay, Google Pay, and limits that rival their KYC counterparts.

No-KYC vs KYC: Full Comparison Table

Here is a direct, data-driven comparison across every factor that matters when choosing between a no-KYC and KYC crypto card.

| Feature | No-KYC Crypto Card | KYC Crypto Card |

|---|---|---|

| Privacy | High — no personal data required | Low — full identity verification required |

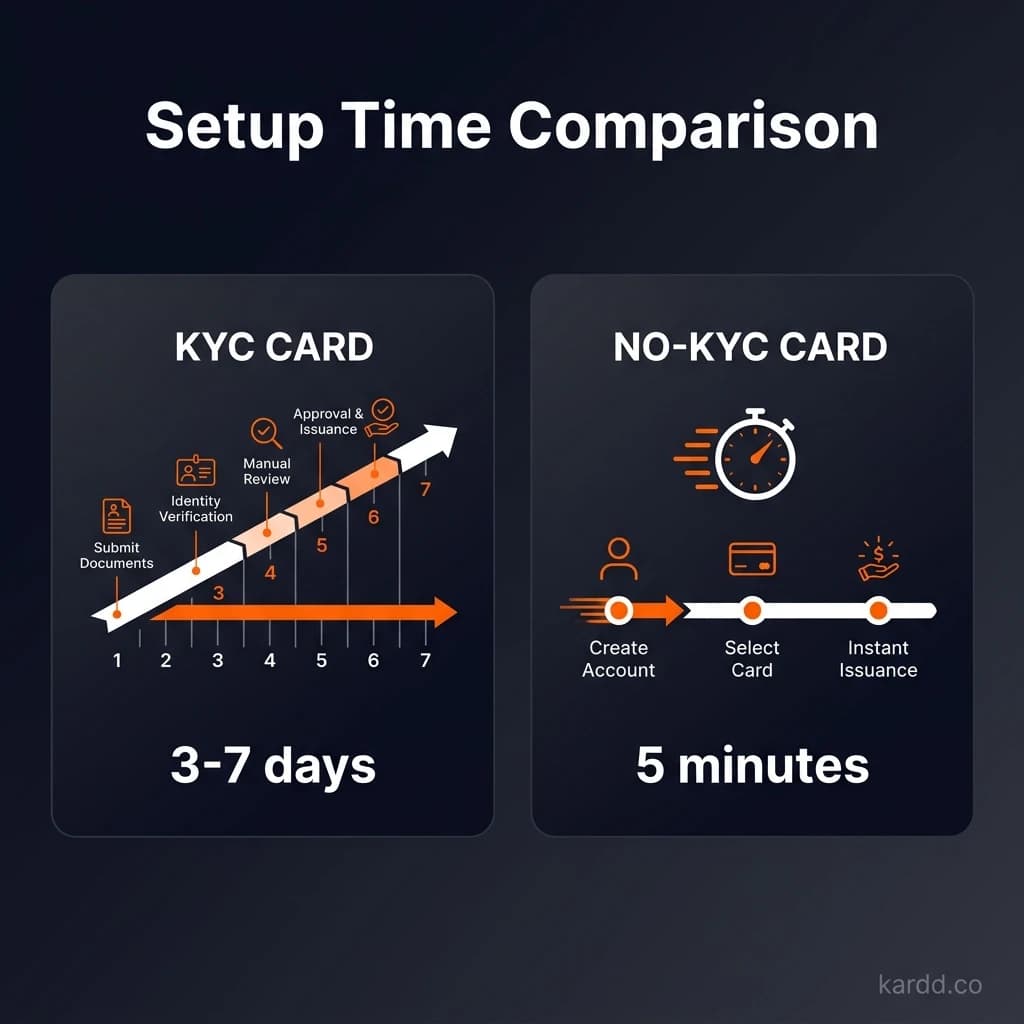

| Setup Speed | Minutes (sometimes seconds) | Hours to days (verification queue) |

| Typical Fees | 1%-5% per transaction or load | 0%-1% per transaction |

| Spending Limits | $500-$100,000/month | $10,000-$50,000+/month |

| Customer Support | Limited (email, Telegram) | Full support (live chat, phone) |

| Platform Stability | Variable — some shut down with little notice | High — regulated entities with banking partners |

| Legal Status | Gray area in most jurisdictions | Fully compliant and regulated |

| Chargeback Protection | None in most cases | Yes — standard card network protections |

| Mobile Pay (Apple/Google) | Select cards only | Widely supported |

| Supported Cryptos | BTC, ETH, USDT, USDC (varies) | Wide range, often 50+ assets |

| ATM Withdrawals | Limited or unavailable | Available with standard limits |

| Account Freeze Risk | Low (no linked identity) | Moderate (compliance-triggered freezes possible) |

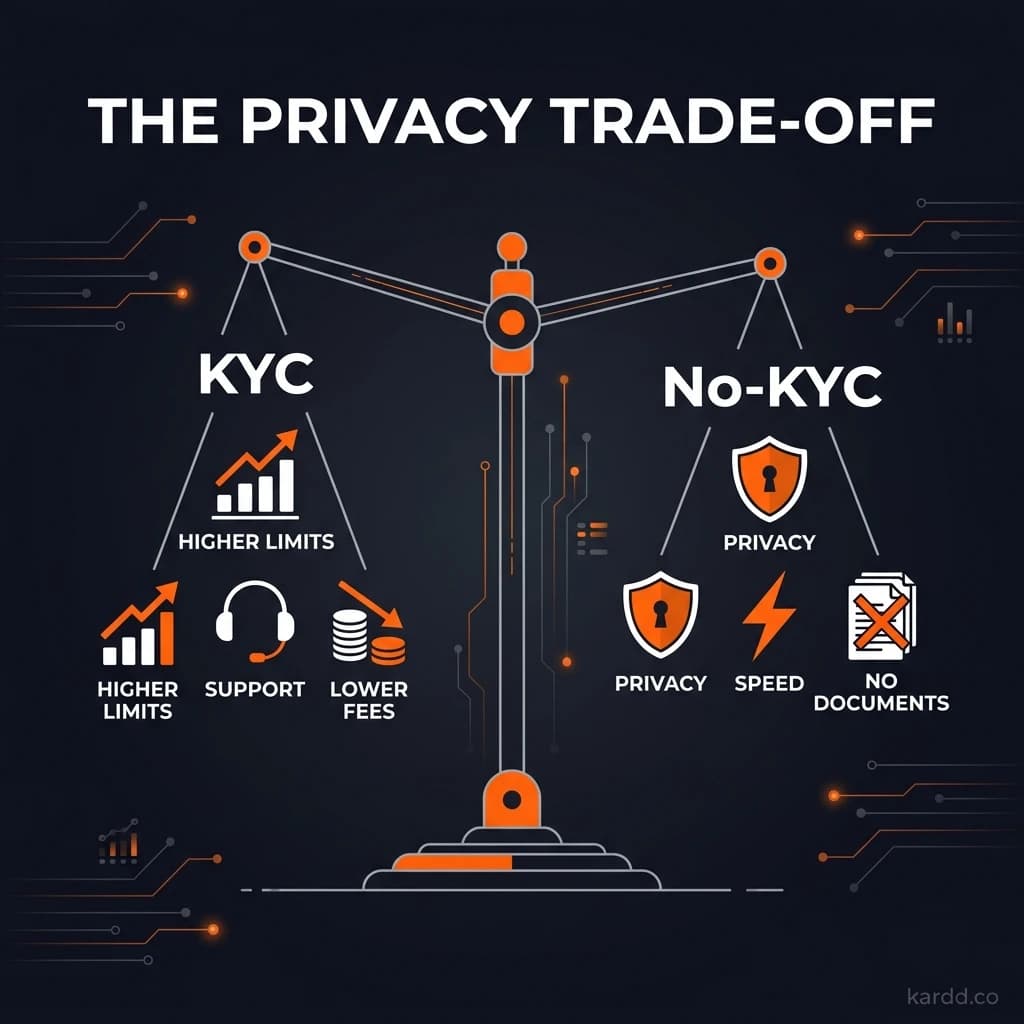

The pattern is clear. KYC cards win on fees, limits, and stability. No-KYC cards win on privacy, speed, and accessibility. Neither is universally better — it depends on your priorities.

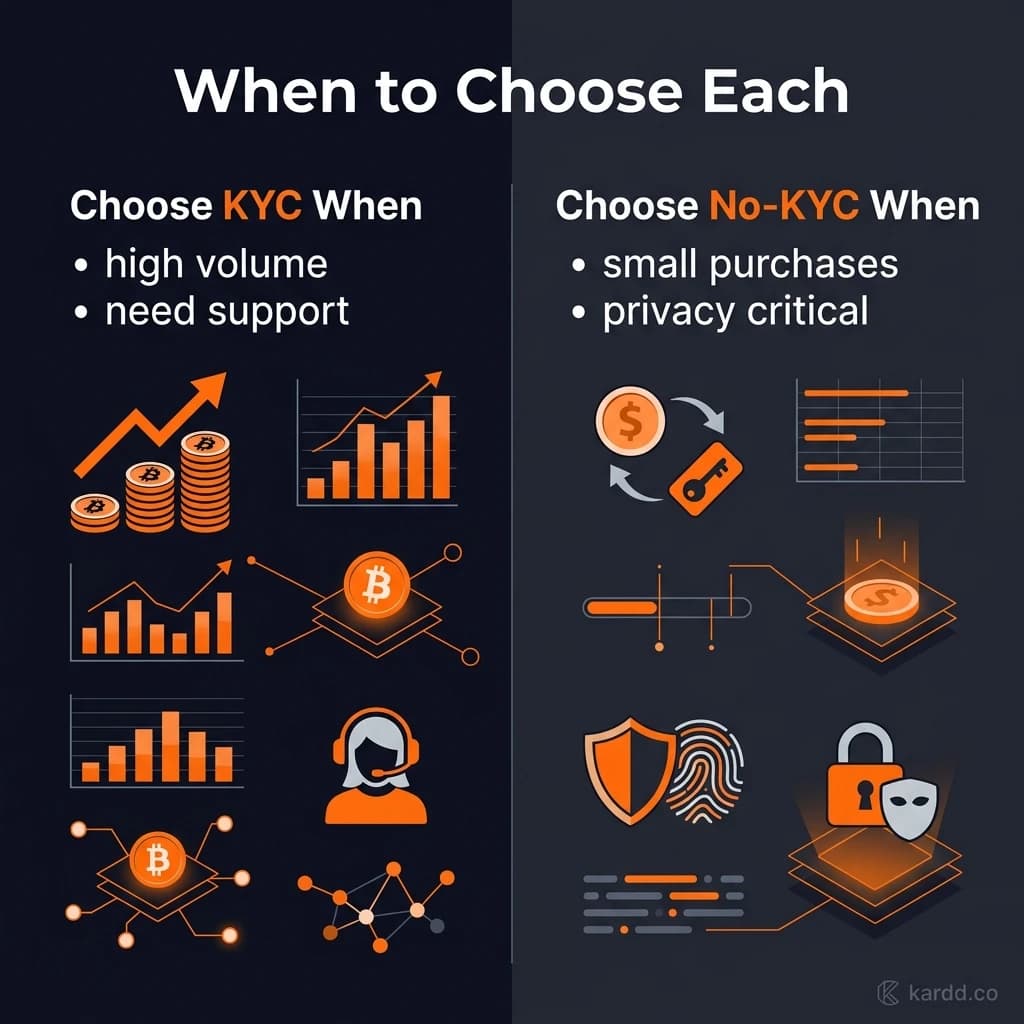

When Should You Use a No-KYC Card?

No-KYC cards are not just for people who “have something to hide.” There are several legitimate, common scenarios where skipping verification is the smarter choice.

Small, Private Purchases

If you are spending $50-$500 on everyday items and do not want that activity tied to your real identity, a no-KYC card is the simplest path. No documents. No waiting. Load USDT, tap your phone, done.

Testing Before Committing

Want to see if spending crypto in the real world actually fits your lifestyle? A no-KYC card lets you try the experience without handing over your passport to a company you have never used before.

Restricted Jurisdictions

Users in countries where KYC-compliant crypto cards are unavailable — or where banking infrastructure makes verification difficult — often rely on no-KYC options as their only viable path to card-based crypto spending.

Privacy-Critical Use Cases

Journalists, activists, freelancers in sensitive industries, and anyone operating in environments where financial surveillance carries real risk. Privacy is not a luxury in these contexts — it is a safety requirement.

Our Top Pick: XKard

For the best overall no-KYC experience in 2026, XKard stands out. Zero identity verification, support for both Apple Pay and Google Pay, limits up to $100,000, and USDT funding on multiple chains.

It is the card we recommend most often to users who want the broadest functionality without touching KYC. Read our full Apple Pay setup guide for details on getting started.

When Does KYC Make More Sense?

KYC is not the enemy. For certain use cases, verified cards are genuinely the better tool.

High-Volume Spending

If you are running $10,000+ per month through a crypto card — whether for business expenses, travel, or daily living — KYC cards offer higher limits and significantly lower fees. That 1%-5% fee gap adds up fast at scale.

Dispute Protection

Charged for something you did not receive? KYC cards give you access to Visa/Mastercard’s chargeback process. No-KYC cards almost never offer this. If you are buying high-ticket items or booking travel, that protection matters.

Long-Term Stability

KYC-compliant issuers have banking relationships, regulatory licenses, and a public reputation to protect. They are far less likely to disappear overnight. If you want a card you can rely on for years, KYC reduces your counterparty risk.

Lowest Possible Fees

Some KYC cards charge zero transaction fees and offer cashback rewards. If cost efficiency is your primary concern and privacy is secondary, a verified card will save you real money over time.

Can You Start No-KYC and Upgrade to KYC Later?

Yes — and this is one of the smartest approaches for users who are still deciding.

Several modern crypto card providers use tiered verification. You start with zero KYC and a basic spending limit. If you later decide you want higher limits, lower fees, or additional features, you can voluntarily submit documents to unlock a higher tier.

How This Works on Popular Cards

XKard offers exactly this model. At the base tier, you get full card functionality with no identity documents — up to $100,000 in limits. Optional KYC unlocks even higher thresholds and additional features for power users. You are never forced to verify.

KAST uses a similar approach. The entry-level card requires no verification. Submitting a government ID unlocks higher daily and monthly limits. The process is optional and can be initiated at any time from the app.

This tiered model is becoming the industry standard. It removes the all-or-nothing choice and lets you calibrate your privacy level to your actual spending patterns.

FAQ

Is a no-KYC crypto card legal?

In most jurisdictions, using a no-KYC crypto card is not illegal for the cardholder. The legal burden typically falls on the issuer to comply with local regulations. However, laws vary by country, and some regions have stricter rules around anonymous financial instruments. Always check your local regulations. For a deeper look at the risks, see our guide on whether no-KYC crypto cards are safe.

Why are no-KYC card fees higher than KYC cards?

No-KYC issuers cannot offset costs through traditional banking partnerships, interchange revenue sharing, or volume-based fee reductions that come with regulatory compliance. The higher fee (typically 1%-5%) covers the cost of operating outside the traditional banking system. Think of it as a privacy premium.

Can my no-KYC card be frozen or shut down?

It is possible but less common than with KYC cards, since there is no linked identity to flag. The bigger risk is the issuer itself shutting down or changing terms. Stick with established providers like XKard that have a track record. Never store large balances on any card — load what you plan to spend.

Which is better for travel — KYC or no-KYC?

For extended international travel, KYC cards are generally more reliable. They offer wider ATM access, chargeback protection for hotel and flight bookings, and less risk of merchant declines. For short trips or supplemental spending, a no-KYC card works fine — especially if it supports mobile pay for contactless transactions.

Conclusion

The no KYC vs KYC crypto card debate is not about picking a winner. It is about matching the tool to the job.

Choose no-KYC when privacy, speed, and accessibility matter most. For most users, XKard delivers the best balance of functionality and anonymity — zero verification, Apple Pay and Google Pay support, and limits that handle real spending.

Choose KYC when you need high limits, dispute protection, and the lowest possible fees.

Choose both if you want the best of each world. Start no-KYC for everyday private spending. Add a KYC card for large purchases and travel. There is no rule that says you can only carry one.

Cards Mentioned in This Guide

Last verified: March 18, 2026. Card details, fees, and KYC requirements may change without notice. Always verify current terms directly with the card issuer before loading funds. Full affiliate disclosure