Best No-KYC Crypto Cards for High-Limit Spending (2026)

Most no-KYC crypto cards cap you at $1,000-$3,000 per month. For users moving serious volume — freelancers paid in USDT, traders taking profits, or businesses operating in crypto — that’s not enough. You need a no-KYC crypto card with high limits that doesn’t force you to hand over your passport.

Good news: options exist. The best no-KYC cards now offer limits from $5,000 to $100,000 per month. Here’s how to access them.

No-KYC Card Limits: The Full Ranking

| Card | Monthly Limit | KYC Level | Top-Up Fee | Mobile Pay |

|---|---|---|---|---|

| XKard Whale | $100,000 | Zero KYC | 2.3% | Apple Pay + Google Pay |

| XKard Standard | $10,000 | Zero KYC | 4.5% | Apple Pay + Google Pay |

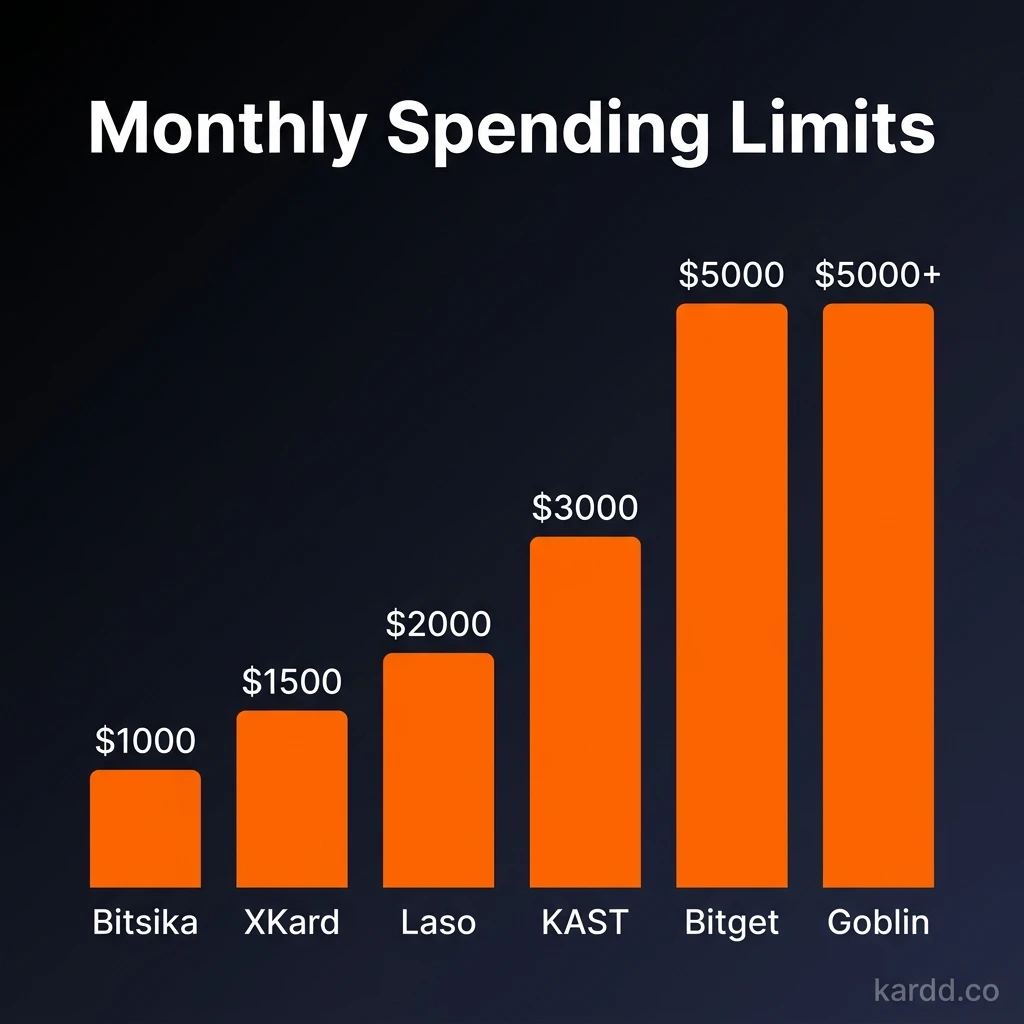

| Goblin Card | $5,000+ | None | 3-4% | No |

| Bitget Wallet | $5,000 | Partial | 1-2% | Google Pay |

| SolCard | $5,000 | Zero KYC | 5% | Apple + Google Pay |

| KAST | $3,000 | Minimal | 2% | Apple Pay |

| COCA Card | $3,000 | Minimal | 2.5% | Apple Pay |

| Bancus | $2,500 | Minimal | 2.5% | No |

| Laso Finance | $2,000 | None | 2-3% | Apple + Google Pay |

| BingCard | $1,000 | Minimal | 1% | No |

| Bitsika | $1,000 | None | 2% | No |

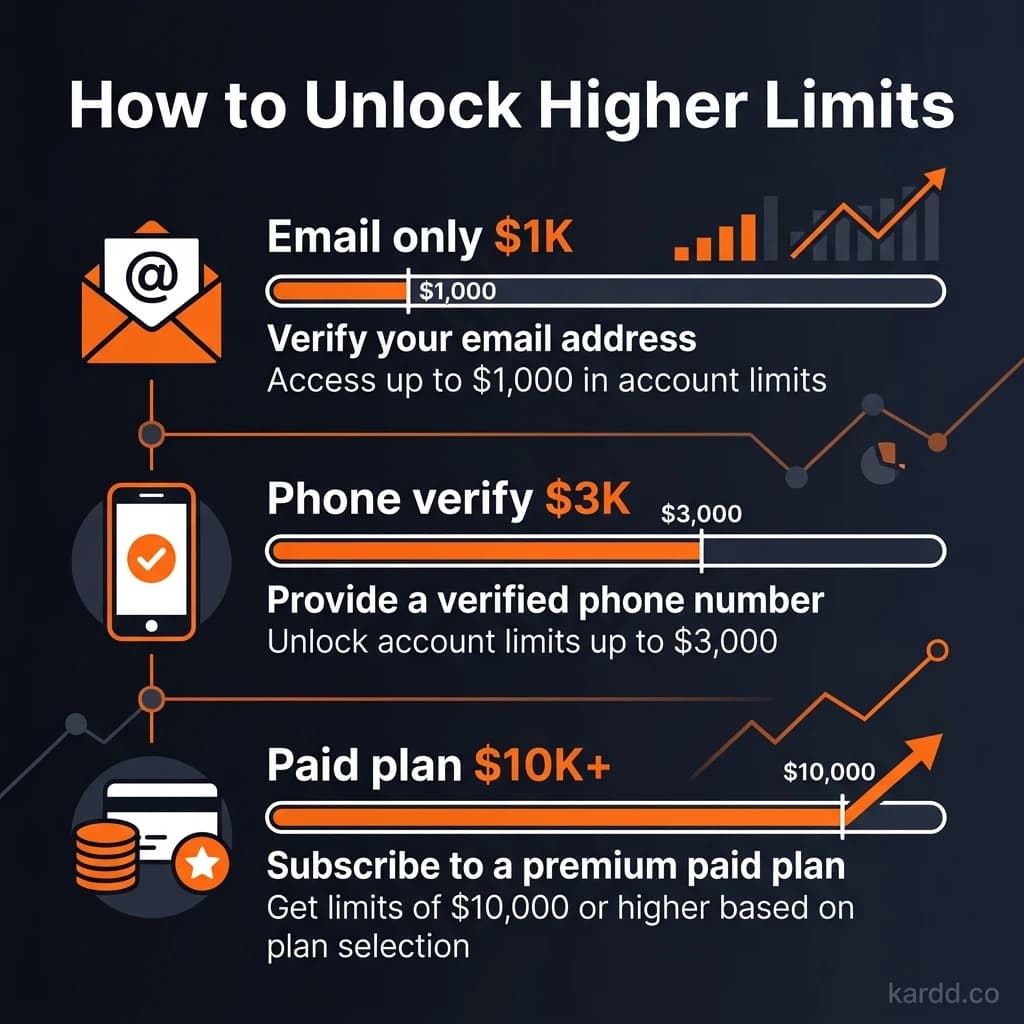

How Limit Tiers Work

No-KYC doesn’t mean one-size-fits-all. Most cards operate on tiered limits based on how much verification you provide:

Tier 1 — Zero verification (email or nothing): $500-$1,000/month. This is the default for BingCard, Bitsika, and basic SolCard.

Tier 2 — Light verification (email + phone): $2,000-$5,000/month. KAST, Laso Finance, and COCA Card operate here.

Tier 3 — Premium zero-KYC (subscription-based): $10,000-$100,000/month. XKard unlocks massive limits through paid tiers rather than identity verification. You pay for access with money, not documents.

This is the key innovation: XKard replaces identity verification with subscription tiers. Higher monthly fee = higher limits, without ever submitting ID.

Best Cards for $5,000+/Month Spending

1. XKard (Best Overall)

The only no-KYC card that scales to $100K/month. Multiple subscription tiers:

- Standard: $108/year, $10K/month, 4.5% reload

- Whale: $588/year, $100K/month, 2.3% reload

The Whale tier’s 2.3% reload fee is actually competitive with partial-KYC cards charging 1-2% when you factor in XKard’s zero FX fee and Apple Pay + Google Pay support. At $10K+/month spending, the effective rate per dollar is lower than most competitors.

2. Goblin Card (Best for Privacy Maximalists)

$5,000+/month with zero verification and the only card accepting Monero (XMR). Physical and virtual options. Higher fees (3-4%) but no annual subscription. Best for users who want maximum anonymity and are willing to pay the privacy premium.

3. Bitget Wallet Card (Best Low-Fee Option)

$5,000/month at just 1-2% top-up. The catch: requires partial KYC (phone verification). If you’re comfortable with a phone number on file, this is the cheapest high-limit option. Google Pay supported, no Apple Pay.

4. SolCard (Best for Solana Users)

$5,000/month on SOL, USDT, and USDC via the Solana network. Zero KYC with Apple Pay and Google Pay. The 5% fee is steep, but for SOL ecosystem users it’s the most native option.

XKard Whale Tier: $100K/Month at Zero KYC

Worth a deeper look because nothing else comes close at this limit level without ID:

- Annual subscription: $588/year ($49/month)

- Top-up fee: 2.3% (lowest of any XKard tier)

- Monthly limit: $100,000

- KYC: Zero — email only

- Networks: Visa + Mastercard

- Mobile: Apple Pay + Google Pay

- Crypto: USDT on BNB Chain and TRON

Effective Cost at $10,000/month

- Top-up: $230 (2.3%)

- Spread: ~$50 (0.5%)

- Annual fee: $49/month

- Total: $329/month (3.29% effective)

At $50,000/month, the annual fee becomes negligible and the effective rate drops to ~2.8%. For high-volume no-KYC spending, this is currently the most cost-efficient option available.

The Trade-Off: Higher Limits = Higher Fees?

Not always. The relationship between limits and fees is more nuanced:

| Volume | Cheapest Option | Effective Rate |

|---|---|---|

| Under $1K/month | BingCard | ~2.5% (1% + spread) |

| $1K-$3K/month | KAST or COCA | ~3% (2-2.5% + spread) |

| $3K-$5K/month | Goblin or SolCard | ~4-5.5% |

| $5K-$10K/month | XKard Standard | ~5% (4.5% + spread + annual) |

| $10K+/month | XKard Whale | ~2.8-3.3% |

The sweet spot is either very low volume (BingCard) or very high volume (XKard Whale). The middle range ($3K-$10K) is the most expensive per dollar.

FAQ

What’s the highest monthly limit on a no-KYC crypto card?

XKard’s Whale tier offers $100,000/month at zero KYC — the highest limit in the no-KYC space. The next highest is Goblin Card at $5,000+/month.

Can I use multiple cards to increase my total limit?

Yes. Many high-volume users spread across 2-3 cards. This also diversifies risk — if one card freezes, you still have access to the others. Just note this creates more points of failure.

Do high-limit no-KYC cards work for business expenses?

They can, but proceed carefully. No-KYC cards don’t issue business receipts or tax documents. For business use, you’ll need to track transactions manually. The lack of chargeback protection also means no recourse on disputed vendor payments.

Is XKard Whale worth the $588/year subscription?

At $10K+/month spending, yes. The 2.3% reload fee saves more than the subscription costs compared to lower tiers. Below $5K/month, the annual fee makes the effective rate too high — stick with Standard or a different card.

Conclusion

High-limit no-KYC spending is possible in 2026, but options narrow quickly above $5,000/month. XKard dominates the high end with its $100K Whale tier, while Goblin Card and Bitget Wallet serve the $5K range.

Compare all card limits

See every no-KYC card ranked by spending limits, fees, and features.

Compare on Kardd.coCards Mentioned in This Guide

Last verified: March 18, 2026. Card details, fees, and KYC requirements may change without notice. Always verify current terms directly with the card issuer before loading funds. Kardd.co is an independent comparison site — we are not affiliated with any card issuer except through publicly available affiliate programs. Full affiliate disclosure